I. Introduction

The Chinese passenger car tire market, the world’s largest, is undergoing a profound transformation in 2025. The market is being reshaped by the accelerated rise of domestic brands, strategic overseas expansion by manufacturers, and powerful new growth drivers stemming from automotive industry trends—particularly new energy vehicles (NEVs) and SUVs.

Part 1: Analysis of Passenger Car Tire Production in China

1.1 Domestic Capacity Planning and Current Status

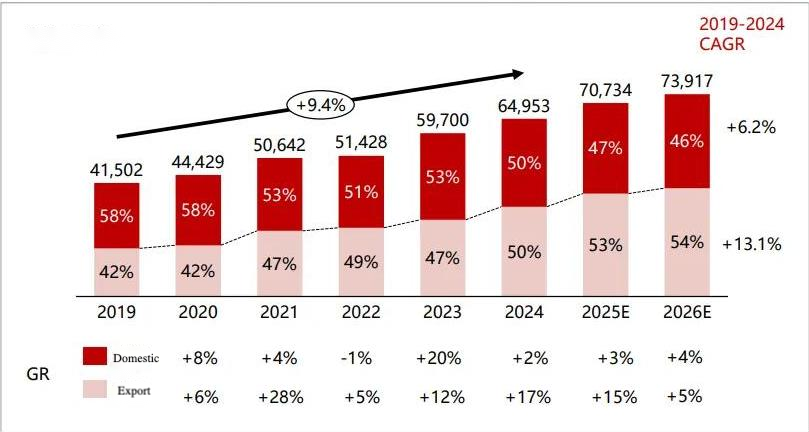

China’s tire industry has transitioned from a phase of rapid capacity expansion to one of structural optimization and regional agglomeration. The production volume of passenger car tires increased from 421 million units in 2019 to a peak of 661 million units in 2024, followed by a minor correction. Output for 2025–2026 is projected to stabilize at around 650 million units annually. Current capacity planning emphasizes technological upgrading, green manufacturing, and intelligent production rather than simple quantitative growth. Leading enterprises are concentrating resources in major industrial clusters (e.g., Shandong, Jiangsu, Zhejiang), enhancing efficiency and competitiveness through scale and synergy.

China’s passenger car tire production from 2020 to 2026

Unit: Ten thousand entries

China’s eight major regions account for 88% of annual passenger car tire production:

1.2 Overseas Expansion and Current Status of Chinese Tire Enterprises

Facing international trade uncertainties and to better serve global markets, leading Chinese tire companies have accelerated their overseas deployment. Strategic layouts in Southeast Asia (e.g., Vietnam, Thailand) and Europe (e.g., Serbia) have been key moves. This not only effectively circumvents trade barriers but also leverages local advantages to enhance global supply chain resilience. For instance, factories in Southeast Asia primarily serve markets in North America and Europe, while European bases strengthen local service and brand presence. Overseas capacity has become a new core growth driver for top Chinese tire companies.

Company | Location | Capacity of PCR (Overseas) |

Sailun Tire | Mexico | 600 |

Cambodia | 1200 | |

Prinx Chengshan Tire | Malaysia | 600 |

Linglong Tire | Serbia | 850 |

Sentury Tire | Spain | 1200 |

Haohua Tire | Vietnam | 1200 |

Firemax | Cambodia | 800 |

Wanli Tire | Cambodia | 1000 |

Double Star Tire | Cambodia | 700 |

Zhongce Rubber | Mexico | Planning |

Thailand | 700 | |

General Science | Thailand | 1000 |

Jinyu Tire | Vietnam | 1000 |

Part 2: Analysis of Passenger Car Tire Market Sales in China

2.1 Industry Development Changes of Passenger Car Tire (2019-2024)

Over the past five years, the China tire market has navigated significant fluctuations, including the impact of the pandemic, volatility in raw material prices, and the structural shift in automotive demand. Overall, the market demonstrated strong resilience. The production scale of semi-steel tires increased from 421 million units in 2019 to a peak of 661 million units in 2024, followed by a slight correction, entering a new phase of steady development.

2.2 Changes in the Domestic Market of Passenger Car Tire

- Rising Market Share of Domestic Brands: In the replacement market, the share of leading domestic brands has significantly increased, driven by substantial improvements in product quality, optimized channel networks, and growing consumer recognition. Consumers are increasingly accepting and preferring high-quality domestic tire brands.

- Rising Market Share of Domestic Brands: In the replacement market, the share of leading domestic brands has significantly increased, driven by substantial improvements in product quality, optimized channel networks, and growing consumer recognition. Consumers are increasingly accepting and preferring high-quality domestic tire brands.

2.3 Changes in the Passenger Car Tire Export Market

Chinese passenger car tire exports have shifted from being “volume-driven” to “volume and value rising together.” Despite facing international trade challenges, exports have maintained growth momentum by virtue of comprehensive cost-performance advantages and flexible market strategies. Exports of mid-to-high-end products from leading enterprises are increasing, and export destinations are becoming more diversified, reducing reliance on any single market.

2.4 Current Rankings and Status of Passenger Car Tire Manufacturers

Based on comprehensive metrics such as production scale, global market share, and brand influence, the first-tier Chinese passenger car tire manufacturers in 2025 mainly include:

Company | Production Site | Capacity (10k pcs/year) | Future (10k pcs/year) |

Linglong | Zhaoyuan, Dezhou, Liuzhou, Hubei, Changchun | 6300 | 1200 |

Zhongce | Hangzhou, Zhejiang; Jintan, Jiangsu | 5900 | 2000 |

Sailun | Qingdao, Dongying, Weifang | 5000 | 2000 |

Youyue Rubber | Shandong | – | 1200 |

Michelin | Shenyang, Shanghai | 2450 | 730 |

Firemax Tyre | Shouguang, Shandong | 800 | 1200 |

Sentury | Qingdao, Shandong | 2500 | 500 |

Kumho Tire | Nanjing, Tianjin, Changchun | 1700 | 140 |

Triangle | Weihai, Shandong | 2000 | – |

Double Coin | Anhui | 1500 | 80 |

Goodyear | Dalian, Kunshan | 2200 | 1000 |

Continental | Hefei | 1750 | – |

Pirelli | Yanzhou, Shenzhou, Jiaozuo | 1400 | – |

Prinx Chengshan | Shandong | 1500 | – |

Yokohama | Hangzhou, Suzhou, Shandong | 900 | 500 |

2.5 Current Market Brand Landscape and Status of Leading Tire Brands

The brand landscape is becoming clearer: international first-tier brands (e.g., Michelin, Bridgestone) firmly hold the high-end market; leading domestic brands are rapidly advancing toward the mid-to-high-end segment; while numerous small and medium-sized brands compete in the low-end market. Leading domestic brands are increasing investment in brand building, enhancing consumer mindshare through technological innovation, quality commitment, and sports marketing, accelerating the transformation from “manufacturing” to “branding.”

China’s passenger car tyre market concentration

Domestic and foreign capital ratio

Red: Domestic capital

Pink: Foreign capital

Part 3: Analysis of Key Market Segments

3.1 Analysis of the Original Equipment (OE) Car Tyre Market

The OE market is the vanguard of technological trends. The most significant change is the rapid increase in the proportion of new energy vehicle (NEV) tires. Tires for NEVs require characteristics such as low rolling resistance, high load capacity, wear resistance, and low noise, posing new challenges and opportunities for tire companies. Leading domestic brands have successfully entered the supply chains of mainstream domestic NEV manufacturers (e.g., BYD, NIO, Xpeng), becoming important partners in automotive industry innovation.

3.2 Analysis of the Replacement Market

The replacement market is the mainstay of industry revenue and profit. Current trends show further segmentation and premiumization. Consumers not only consider price but also pay more attention to safety performance, fuel efficiency, comfort, and durability. Online sales channels (e-commerce) are playing an increasingly important role, and the integration of “online purchase + offline installation” services has become standard. Tires tailored for SUVs and high-performance models are hot-selling categories.

3.3 Analysis of the Winter Tire Market

The winter tire market has evolved from”regional necessity” to “national safety demand.” With increasing consumer awareness of driving safety and the impact of extreme weather, sales in winter tire markets in central and southern China are growing significantly. Domestic brands are leveraging their cost-performance and channel advantages to accelerate product development and market penetration in this segment, challenging the dominance of traditional international winter tire brands.

Winter tires account for 90% of tire usage in China’s five major regions:

V. Conclusion and Outlook

Looking ahead to 2025 and beyond, China’s passenger car tire market will present the following key trends:

Domestic brands will continue to rise, further compressing the market space of international second- and third-tier brands and forming a direct competitive relationship with first-tier international brands.

Product innovation will center around NEVs and intelligence, with smart tires and airless tires expected to move from concept to initial commercialization.

Green and sustainable development will become a mandatory requirement, driving the entire industry chain toward energy conservation, emission reduction, and circular economy.

Globalized layout will become the norm for leading enterprises, forming a dual-engine development model of “domestic headquarters + overseas bases.”

Overall, the Chinese passenger car tire industry is steadily transitioning from a “large manufacturing country” to a “strong manufacturing country” during this round of profound restructuring, and its global influence is set to reach new heights.

Forlander stands out as a leading tire brand in China, offering a wide range of PCR tire sizes and tread patterns to meet your needs. We invite you to reach out to us for our comprehensive product catalog. Whether you have questions or specific requirements regarding tires, our team is here to assist you. Don’t hesitate to contact us!